The market for foreign plays, which had been almost monopolized by China, was in the midst of a brutal cut-off.

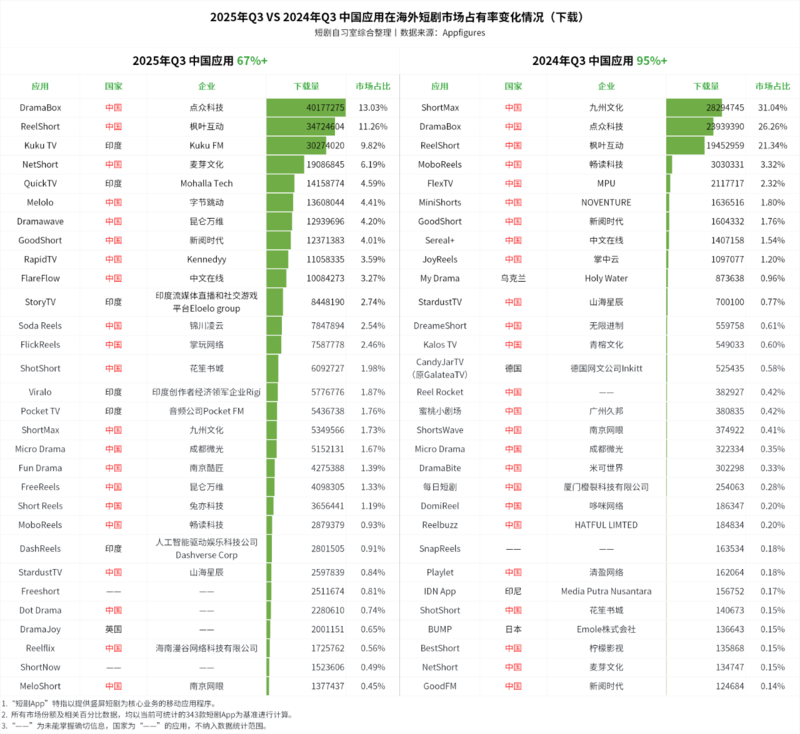

According to the latest data, in the third quarter of 2025, the overseas short play market contributed 67 per cent + to the TOP30 application.

This figure, which appears to be strong, represents a total decline of 28 percentage points compared with 95 per cent in the same period in 2024.

The war has changed: India has applied a collective run, the Japanese-Korean platform has turned to its own IP to build a content barrier, and there is an influx of global players like Ukraine and Germany.

At the same time, leading giants such as Disney, Amazon, and the United States Actors Union are entering the arena strongly and are reshaping industry rules and competition thresholds.

Former leaders are now in multidimensional competition. How do we break this? How can you hold your place at the new card table?

Entering the entertainment giant, the “median” dropped by almost 30%.

The overseas shorts market is still making cakes.

In the third quarter of 2025, the overseas shorts market received more than 308 million downloads, with revenues of $647 million, an average increase of over 12 per cent.

However, behind this boom, the voice of Chinese players is declining.

The share of downloads generated by the Chinese application in the download volume Top 30 dropped by 28 per cent, from 95 per cent in the third quarter of last year to 67 per cent in the same period. At the same time, the number of applications in China had been reduced from 25 to 21.

The change in pattern lies not only in the shrinking share, but also in the fact that the challenger has escalated from a “scramble” to a “group army”.

Last year’s overseas application on the list was unclimate, and this year India’s single-market application was strong at six seats, with more than 21 per cent downloads, with Kuku TV heading for the second ReelShort.

The Chinese camp also experienced a brutal shuffle.

Although Dramabox and ReelShort are still at the forefront, their combined market share has been cut from nearly half (47.6 per cent) to 24.3 per cent. Last year’s top shot of Shot Max fell out of the top 10.

So, the overseas shortshow market has completely set off from the old era of China’s giant monopoly, entering a new phase of global local players’ competition for shares.

Changes in download volume Top30 application pattern

Homecomings, giants, foreign forces.

If, last year, small and large players tested water sporadically, this year is the year of a collective effort by overseas indigenous enterprises.

I. COMMON APPLICATION COMPANY

The first is the upgrading of the player ‘ s identity.

While 2024 was a test site for digital content and technology companies, by 2025, “regular forces” such as Fuji TV Japan, JTBC Korea and NBC Globe USA had entered the field. In the near future, the MirroCo and Verza TV platforms with a Hollywood background are ready to go. There has been a marked rise in the short play competition pattern.

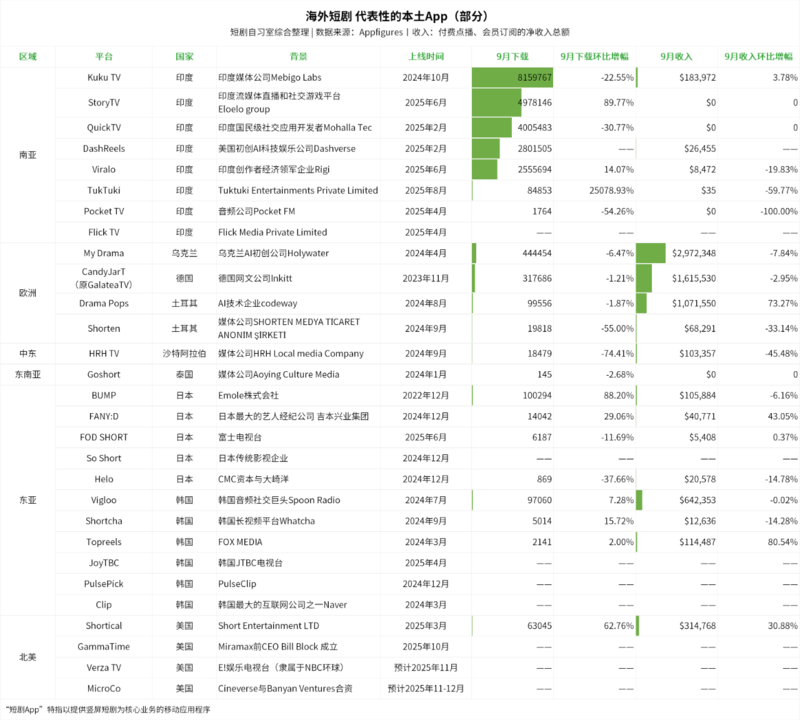

The more significant change is the collective rise of Indian applications.

Kuku TV, StoyTV, QuickTV, and Villalo have been online for less than a year, reaching a monthly average of 1 million downloads. Of these, StoyTV was downloaded for nearly 5 million months in just four months, demonstrating the amazing penetration of indigenous content.

Overseas Play App Case Inventory

Indigenous production “outside alliances”

A new force, created by the indigenous media giants, production companies, and the “strength of power” of the technology platform, is emerging to create a new ecology that does not depend on the Chinese team.

The overseas IP has started to translate “short-duperization”.

Telemundo Studios, the leading American-Speaker in Spanish, directly adapted his own hot opera set into a short play; in Korea, Vigloo, in collaboration with the American-run media platform PASSIONFLIX, adapted the latter ‘ s hot series, ” Amy Benson ‘ s Secret Life ” , into a stand-off short play.

Capacity and channels are also forming transnational alliances.

The British Spirit Studios and the German Night Train Media formed a full project team from the writer to the distribution; the old Mumbai production company, O.U.T. Media, plans to produce more than 100 units a year and actively engage in the Middle East market.

Most notably, the old American video group Fox Entertainment is involved.

Not only did Fox invest in the Ai shortshow company, Holywater, but it announced ambitious plans to produce over 200 shorts for its platform My Drama within two years and to develop on Fox’s IP.

More recently, the company constructed a three-pronged digital content ecosystem through a cooperation agreement with Harper Collins Publicers and the acquisition of Meet Cute, a popular audio-visual platform. This layout has enabled it to have both greater IP resources and more solid data support for the development of the short play.

An inventory of cases of short play production by overseas local companies

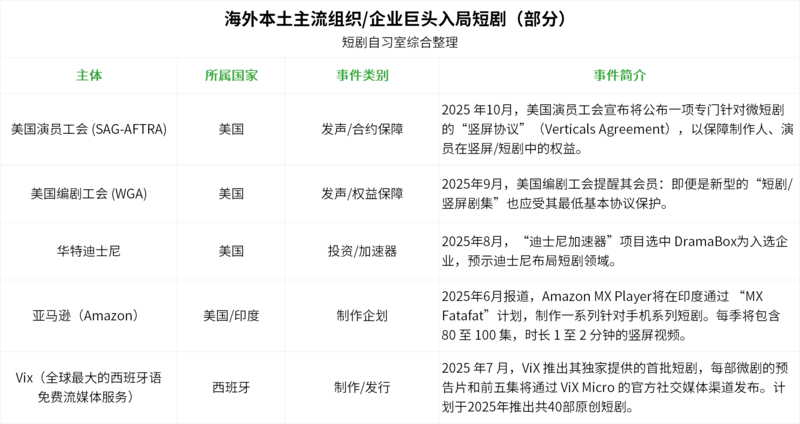

The mainstream forces that have shaped the United States film and film resources have ended.

Recently, the American Actors ‘ Union (SAG-AFTRA) has spoken back and forth with the American Editors ‘ Union (WGA) to launch negotiations and initiatives on the protection of the rights and interests of short play creators, signalling that the American short play market is about to be reshaped.

At the same time, the entertainment giants with top IP and capital are moving up and up.

Disney chose DramaBox through the accelerator project to release the strategic intent of the short-run ecology, while Amazon launched the “MX Fatafat” project in India to carry out a downscaling with indigenous content.

The world’s largest Spanish-language media, VIX, has also announced the goal of producing 40 original dramas per year and has fully integrated it into its mainstream content system.

There are indications that the short play has been upgraded from an emerging track to a central arena for the global mainstream entertainment industry. The question then emerges: How many more seats can Chinese companies occupy in this global battle?

Who has the “right to develop” the gold mine in the second half of the war?

The competition in the short play industry, which is really about the content.

The establishment of systematic and sustainable content production lines overseas has become the first step for the Chinese platform to establish its foothold in the local market.

At the beginning of China’s short play, the layout of the industrial chain followed a clear market logic: first, South-East Asia, where costs were manageable, then North America, where production resources were concentrated, and then Japan, Korea, where the content industry matured.

This method did work around 2024, and the Chinese team, with its experience of production and ablution methods, opened up the situation in several markets.

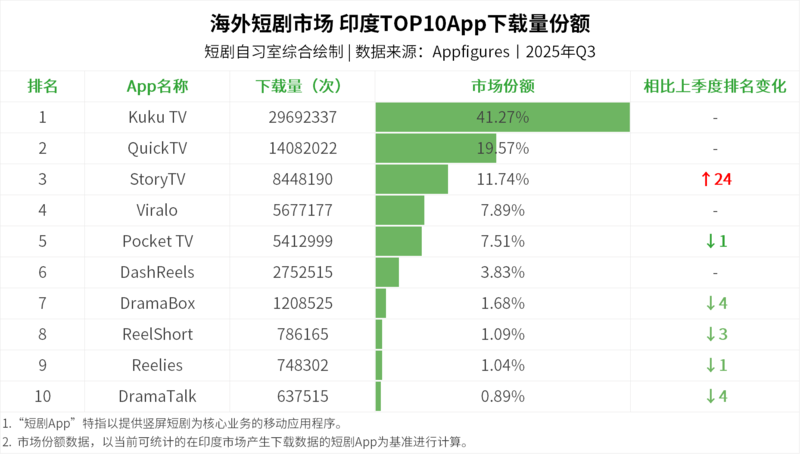

This year, there has been a new change — a delay in seeing Chinese enterprises in India’s top download.

It is clear that it is difficult for the Chinese team to build content production lines in India itself.

On the one hand, production costs are a real challenge.

According to Yoyo, “Indian short play budget is very low, less than one third of the cost of Chinese short play production, and is almost accessible only to local teams”. She added that local teams, with their cost advantages, had taken over the main capacity and had worked closely with local platforms to build up the billions of dollars that they would broadcast.

The Chinese production companies, if they want to produce on the ground in India, will have to bear the additional costs of sending and travelling, making it difficult to keep the overall budget at the level of local teams, and few of them are willing to “eat crabs”.

On the other hand, India has a highly complex linguistic and cultural structure.

Twenty-two official languages are parallel, and religious beliefs and cultural practices vary greatly from one region to another, making their content market “barrier” a threshold that the Chinese team cannot reach into the Indian market.

Against this background, the Indian market has grown this year, with a rare absence of Chinese applications that have been at the top of major markets. In the third quarter of this year, more than 90 per cent of the downloads from Indian short play applications were occupied by indigenous applications, while ReelShort and DramaBox received only a 3 per cent share.

However, access to the Indian market is not complete.

According to Yang Liu, the Indian short play production company is eager to learn about the Chinese short play model, which they want to adapt to the Chinese script and to learn from. Perhaps the Chinese team in the later stages can enter the market through the Union Communism.

In the US-Japan mainstream market, which has long been in place, the Chinese team is faced with another round of competition.

The low cultural barriers in the United States market, as well as the relative lag in industry awareness, provided early access opportunities for Chinese application and production teams. However, as the market potential became apparent, local video giants and mainstream forces began to end, and industry rules had to be reshaped.

The founder of the Catalytic Film Foundation anticipated that “a regulatory entry would raise production and distribution costs, and trade unions would be the first threshold and future issuance regulation would be the real challenge”. If Chinese enterprises are to be established in the long term, they must move towards regularization and capitalization. It will also eliminate a number of under-represented platforms.

The Japanese and Korean markets are more like the “Professional League” of the best.

In both markets, when the industry was conscious, in 2024, the local platform was centralized and entered from traditional television stations to professional content companies. More importantly, Japan and Korea have mature animation, video and deep IP reserves that create a natural barrier to their status.

Here, the Chinese team is more like a “tactical coach” hired to teach one or two lessons from past experience. However, once the local team has mastered tactics, the Chinese team’s position will be tested.

The head of Korea’s local production company, KORTOP Media, states: “Vigloo and other platforms are focusing on developing their own IP and scripts, not exclusively on Chinese scripts.”

In the face of these gold-filled hills, it is still not known whether Chinese players can hold on to the “excavation rights”.

Ninety percent of the income is still in hand.

However, the failure of downloads does not mean a loss of income.

On the contrary, in terms of the income structure, Chinese enterprises continue to dominate market rules.

This year, in the TOP30 application, applications from China contributed 93.52 per cent, almost the same as in the same period last year, when 94.84 per cent. ReelShort, DramaBox, etc., remain well-established.

Change in income Top30 application pattern

Perhaps the Chinese team’s strength has not yet been shaken, and we are still present and have the right to speak.

As Jung-hyun said: “We Chinese took the lead in this mountain, defining the way in which the industry plays. Today, global capital and corporate entry is just helping us raise the water level of the entire market.”

Of course, if we are to remain in a good position as the creators of the product and the definition of the rule, we must clearly position ourselves strategically – – Will the capital game continue to pursue short-term flows, or will it be the long-term path to deep-drop content and build IP values? Are you a co-worker or a player?

The choice is not good or bad, and whatever path the player chooses will drive the industry forward.

It’s a different choice, and it leads to a different fate.